S-1/A: General form for registration of securities under the Securities Act of 1933

Published on February 3, 2026

Table of Contents

As filed with the Securities and Exchange Commission on February 3, 2026.

Registration No. 333-292265

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ARKO Petroleum Corp.

(Exact name of registrant as specified in its charter)

| Delaware | 5172 | 39-3168808 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

8565 Magellan Parkway

Suite 400

Richmond, Virginia 23227-1150

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Arie Kotler

President and Chief Executive Officer

8565 Magellan Parkway

Suite 400

Richmond, Virginia 23227-1150

(804) 730-1568

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Drew M. Altman, Esq. Win Rutherfurd, Esq. Greenberg Traurig, P.A. 333 S.E. 2nd Avenue, Suite 4400 Miami, Florida 33131 (305) 579-0500 |

Maury Bricks General Counsel ARKO Petroleum Corp. 8565 Magellan Parkway Suite 400 Richmond, Virginia 23227-1150 (804) 730-1568 |

Stelios G. Saffos, Esq. Michael Benjamin, Esq. Kaj P. Nielsen, Esq. Latham & Watkins LLP 1271 Avenue of Americas New York, NY 10020 (212) 906-1200 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | Subject to Completion | Dated February 3, 2026 |

10,500,000 Shares

ARKO Petroleum Corp.

Class A Common Stock

This is the initial public offering of shares of Class A common stock of ARKO Petroleum Corp. We are offering 10,500,000 shares of our Class A common stock.

Prior to this offering, there has been no public market for our Class A common stock. We anticipate that the initial public offering price will be between $18.00 and $20.00 per share. We have applied to list our Class A common stock on the Nasdaq Stock Market LLC (“Nasdaq”) under the symbol “APC.”

We will have two classes of common stock outstanding after this offering: Class A common stock and Class B common stock. Each share of Class A common stock entitles its holder to one vote on all matters presented to our stockholders generally. All of our Class B common stock, which we do not intend to list on any stock exchange, will be held indirectly by ARKO Corp. (“ARKO Parent”), our parent company, through one or more subsidiaries. Each share of Class B common stock entitles ARKO Parent to five votes on all matters presented to our stockholders generally. Immediately following this offering, the holders of our Class A common stock will collectively hold 23.1% of the economic interests in us and 5.7% of the voting power in us, and ARKO Parent will hold the remaining 76.9 % of the economic interests and 94.3% of the voting power in us. As a result of ARKO Parent’s ownership of a majority of our outstanding voting power, ARKO Parent will have the ability to determine all matters requiring approval by our stockholders, including the election of our directors, amendment of our governing documents, and approval of certain major corporate transactions, and we will be a “controlled company” within the meaning of the corporate governance rules of Nasdaq; however, we do not currently expect or intend to rely on the “controlled company” exemptions from certain corporate governance requirements. See “Management—Controlled Company Exemptions” and “Risk Factors—Risks Related to Ownership of our Class A Common Stock and this Offering—We will be a “controlled company” within the meaning of the rules of Nasdaq and, as a result, will qualify for, and may in the future rely on, exemptions from certain corporate governance requirements. You will not have the same protections afforded to stockholders of companies that are subject to such requirements.”

INVESTING IN OUR SECURITIES INVOLVES A HIGH DEGREE OF RISK. SEE “RISK FACTORS” BEGINNING ON PAGE 35 TO READ ABOUT FACTORS YOU SHOULD CONSIDER BEFORE BUYING SHARES OF OUR CLASS A COMMON STOCK.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||

| Initial public offering price | $ | $ | ||

| Underwriting discounts and commissions (1) | $ | $ | ||

| Proceeds to us, before expenses | $ | $ |

| (1) | We have agreed to reimburse the underwriters for certain expenses in connection with this offering. See “Underwriting (Conflicts of Interest).” |

We have also granted the underwriters an option for a period of 30 days to purchase up to an additional 1,575,000 shares of our Class A common stock on the same terms set forth above to cover over-allotments, if any. See “Underwriting (Conflicts of Interest).”

At our request, the underwriters have reserved up to 5% of the shares of Class A common stock offered by this prospectus for sale, at the initial public offering price, to certain individuals associated with us. See “Underwriting (Conflicts of Interest)—Directed Share Program.”

Delivery of the shares of Class A common stock will be made on or about , 2026.

| UBS Investment Bank | Raymond James | Stifel |

| Mizuho | Capital One Securities |

The date of this prospectus is , 2026.

Table of Contents

| 1 | ||||

| 3 | ||||

| 4 | ||||

| 26 | ||||

| 31 | ||||

| 35 | ||||

| 67 | ||||

| 70 | ||||

| 71 | ||||

| 73 | ||||

| 75 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

82 | |||

| 118 | ||||

| 138 | ||||

| 145 | ||||

| 161 | ||||

| 168 | ||||

| 175 | ||||

| 178 | ||||

| 180 | ||||

| 188 | ||||

| 193 | ||||

| 204 | ||||

| 204 | ||||

| F-1 | ||||

Neither we nor any of the underwriters have authorized anyone to provide any information or make any representations other than those contained in this prospectus or in any free writing prospectus filed with the Securities and Exchange Commission (the “SEC”). Neither we nor any of the underwriters take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of Class A common stock only in jurisdictions where such offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the Class A common stock. Our business, financial condition, results of operations and prospects may have changed since such date.

For investors outside of the United States, neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about, and to observe any restrictions relating to, this offering and the distribution of this prospectus outside of the United States.

Through and including , 2026 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

i

Table of Contents

As used in this prospectus, unless the context otherwise indicates, any reference to “ARKO Petroleum,” “APC,” “our Company,” “the Company,” “us,” “we” and “our” refers, prior to the completion of the Transactions (as defined herein), including this offering, to the operations that primarily comprise the operations of ARKO Parent’s wholly owned subsidiaries GPM Empire, LLC, a Delaware limited liability company formed in 2020, and GPM Petroleum LP, a Delaware limited partnership formed in 2015, which includes ARKO Parent’s Wholesale and Fleet Fueling businesses and the supply of fuel to substantially all of ARKO Parent’s retail convenience stores that sell fuel (collectively, the “Contributed Businesses”), and after the completion of the Transactions, including this offering, refers to ARKO Petroleum Corp., a Delaware corporation and the issuer of the shares of Class A common stock offered hereby, together with its consolidated subsidiaries and the operations that comprise the Contributed Businesses. References in this prospectus to “ARKO Parent” or “Parent” refer to ARKO Corp., a Delaware corporation, and its consolidated subsidiaries. We sometimes refer to our Class A common stock and our Class B common stock collectively as “common stock.”

Basis of Presentation

Except as otherwise disclosed in this prospectus, the historical combined financial statements and summary condensed combined financial data and other financial information included elsewhere in this prospectus are those of the Contributed Businesses, and have been prepared in U.S. dollars in conformity with accounting principles generally accepted in the United States (“GAAP”), except for the presentation of certain non-GAAP measures as discussed below. The Contributed Businesses’ historical combined financial statements have been prepared on a stand-alone basis and are derived from the consolidated financial statements and accounting records of ARKO Parent. The combined financial statements reflect the historical results of operations, financial position and cash flows of the Contributed Businesses and the allocation of certain ARKO Parent operating and corporate expenses relating to the Contributed Businesses based on the historical financial statements and accounting records of ARKO Parent. Accordingly, if the Contributed Businesses had operated as a stand-alone entity, its results may have differed materially from those presented in these combined financial statements. In the opinion of management, the assumptions underlying the Contributed Businesses’ historical combined financial statements, including the basis on which the expenses have been allocated from ARKO Parent, are reasonable.

Non-GAAP Financial Measures

In this prospectus, we present certain financial measures that are not calculated in accordance with accounting principles generally accepted in the United States of America, referred to herein as “non-GAAP.” You should review the reconciliation and accompanying disclosures carefully in connection with your consideration of such non-GAAP measures and note that the way in which we calculate these measures may not be comparable to similarly titled measures employed by other companies. Specifically, we make use of the non-GAAP measures “EBITDA,” “Adjusted EBITDA,” “Discretionary Cash Flow,” “Net Debt” and the “Ratio of Net Debt to Adjusted EBITDA.”

EBITDA, Adjusted EBITDA, Discretionary Cash Flow, Net Debt and the Ratio of Net Debt to Adjusted EBITDA have been presented in this prospectus as supplemental measures of financial performance or liquidity that are not required by, or presented in accordance with, GAAP. We use EBITDA and Adjusted EBITDA for operational and financial decision-making and believe these measures are useful in

1

Table of Contents

About This Prospectus

evaluating our performance because they eliminate certain items that we do not consider indicators of our operating performance. EBITDA and Adjusted EBITDA are also used by many of our investors, securities analysts, and other interested parties in evaluating our operational and financial performance across reporting periods. We believe that the presentation of EBITDA and Adjusted EBITDA provides useful information to investors by allowing an understanding of key measures that we use internally for operational decision-making, budgeting, evaluating acquisition targets, and assessing our operating performance. Discretionary Cash Flow is a liquidity measure we and third parties, such as industry analysts, investors, lenders, rating agencies and others, use to assess our ability to internally fund our acquisitions, pay distributions, and service or incur additional debt. Net Debt is used by management to measure the effective level of our indebtedness. The Ratio of Net Debt to Adjusted EBITDA is an important measure used by our management to evaluate our access to liquidity, and we believe it is a representation of our financial strength. The Ratio of Net Debt to Adjusted EBITDA is also frequently used by investors and credit rating agencies to analyze our operating performance. EBITDA, Adjusted EBITDA, Discretionary Cash Flow, Net Debt and the Ratio of Net Debt to Adjusted EBITDA should not be considered as alternatives to any financial measure derived in accordance with GAAP, including net income (loss). The presentations of these non-GAAP measures have limitations as analytical tools and should not be considered in isolation, or as a substitute for the analysis of, our results as reported under GAAP. Because not all companies use identical calculations, the presentations of non-GAAP measures may not be comparable to other similarly titled measures of other companies and can differ significantly from company to company. For a discussion of the use of these measures and a reconciliation of the most directly comparable GAAP measures, see “Summary—Summary Condensed Combined Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Use of Non-GAAP Financial Measures.”

2

Table of Contents

Unless otherwise indicated, information contained in this prospectus concerning our industry, competitive position and the markets in which we operate is based on information from independent industry and research organizations, other third-party sources and management estimates. Management estimates are derived from publicly available information released by third-party sources, as well as data from our internal research, and are based on assumptions made by us upon reviewing such data, and our experience in, and knowledge of, such industry and markets, which we believe to be reasonable. Any industry forecasts are based on data (including third-party data), models and experience of various professionals and are based on various assumptions, all of which are subject to change without notice. In addition, projections, assumptions and estimates of the future performance of the industry in which we operate and our future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described in “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.” These and other factors could cause results to differ materially from those expressed in the projections, assumptions and estimates made by the independent parties and by us.

3

Table of Contents

This summary highlights selected information from this prospectus and does not contain all of the information that is important to you in making an investment decision. This summary is qualified in its entirety by the more detailed information included elsewhere in this prospectus. Before making your investment decision with respect to our Class A common stock, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and notes thereto included elsewhere in this prospectus. Some of the statements in this prospectus constitute forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements.”

In this prospectus, unless the context otherwise indicates, any reference to “ARKO Petroleum,” “APC,” “our Company,” “the Company,” “us,” “we” and “our” refers, prior to the completion of the Transactions, including this offering, to the operations that primarily comprise the operations of ARKO Parent’s wholly owned subsidiaries GPM Empire, LLC, a Delaware limited liability company formed in 2020 (“GPME”), and GPM Petroleum LP, a Delaware limited partnership formed in 2015 (“GPMP”), which includes ARKO Parent’s Wholesale and Fleet Fueling Businesses and the supply of fuel to substantially all of ARKO Parent’s retail convenience stores that sell fuel (collectively, the “Contributed Businesses”), and after completion of the Transactions, including this offering, to ARKO Petroleum Corp., the issuer of the shares of Class A common stock offered hereby, together with its consolidated subsidiaries and the operations that comprise the Contributed Businesses. Our historical financial results as part of ARKO Parent contained in this prospectus may not be indicative of what our financial results may be in the future as a publicly-traded company that is no longer wholly owned by ARKO Parent or what our financial results would have been had we been such a company during the historical periods presented.

About ARKO Petroleum Corp.

We are a growth-oriented, fuel distribution company and one of the largest wholesale fuel distributors by gallons in North America, supplying customers in more than 30 states across the Mid-Atlantic, Midwestern, Northeastern, Southeastern, and Southwestern United States (“U.S.”). We were formed by ARKO Parent (Nasdaq: ARKO), one of the largest convenience store operators in the U.S. We primarily engage in the fee-based wholesale distribution of motor fuel to the retail sites operated by ARKO Parent that sell fuel (“ARKO Retail,” “ARKO Retail Sites” or “related party sites”) and to third-party dealers under long-term contracts, and we sell fuel at our fleet fueling locations. One of our key business objectives is to make quarterly cash distributions to stockholders and, over time, increase our quarterly cash distribution.

We operate through three reportable segments:

| i. | Wholesale: Our Wholesale segment distributes fuel to gas stations operated by third-party dealers, sub-wholesalers, and bulk and spot purchasers (e.g., commercial, government, industrial businesses, and rack buying dealers), on either a cost-plus or a consignment basis, generally pursuant to long-term contracts. |

| ii. | Fleet Fueling: Our Fleet Fueling segment includes the operation of proprietary and third-party cardlock locations (unstaffed fueling locations that serve commercial vehicle fleets) that |

4

Table of Contents

Prospectus Summary

| primarily sell fuel to commercial and municipal entity customers, and we also generate revenue through commissions from the sale of fuel using proprietary fuel cards that provide customers access to a nationwide network of fueling sites. APC is one of the largest cardlock operators in the U.S. and maintains a leading position in the Mid-Atlantic region. |

| iii. | GPMP: Our GPMP segment sells and supplies fuel to substantially all of the ARKO Retail Sites at our cost of fuel plus a fixed margin, and the GPMP segment charges a fixed fee to certain of the ARKO Retail Sites that are not supplied by us. In addition, the GPMP segment includes intercompany transactions which are eliminated in the combined financial statements contained in this prospectus. |

For the year ended December 31, 2024 and the nine-month period ended September 30, 2025, we distributed 2.1 billion gallons and 1.5 billion gallons, respectively, of fuel to our customers. We purchase our fuel from independent refining companies and major oil companies and then distribute it to customers using third-party haulers, and in certain cases our own trucks. We believe we have limited exposure to fluctuating commodity prices because we generally pass the cost of the fuel we distribute through to our customers. In addition, we are able to generate larger fuel margins (i) under consignment distribution arrangements with third-party dealers, where we maintain control of the fuel inventory and retail fuel pricing, and (ii) on fuel sales at our cardlock locations, compared to fuel supply arrangements.

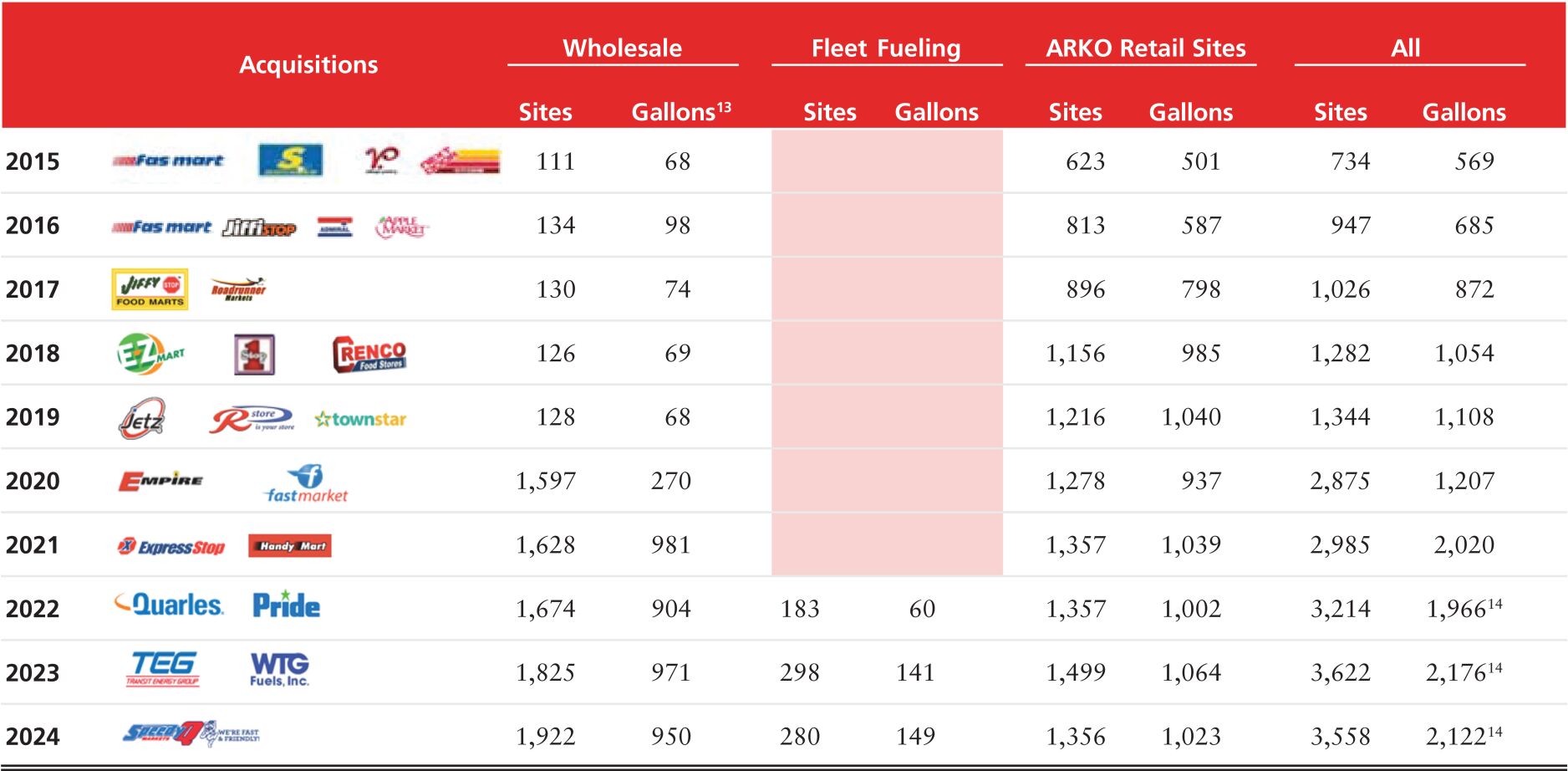

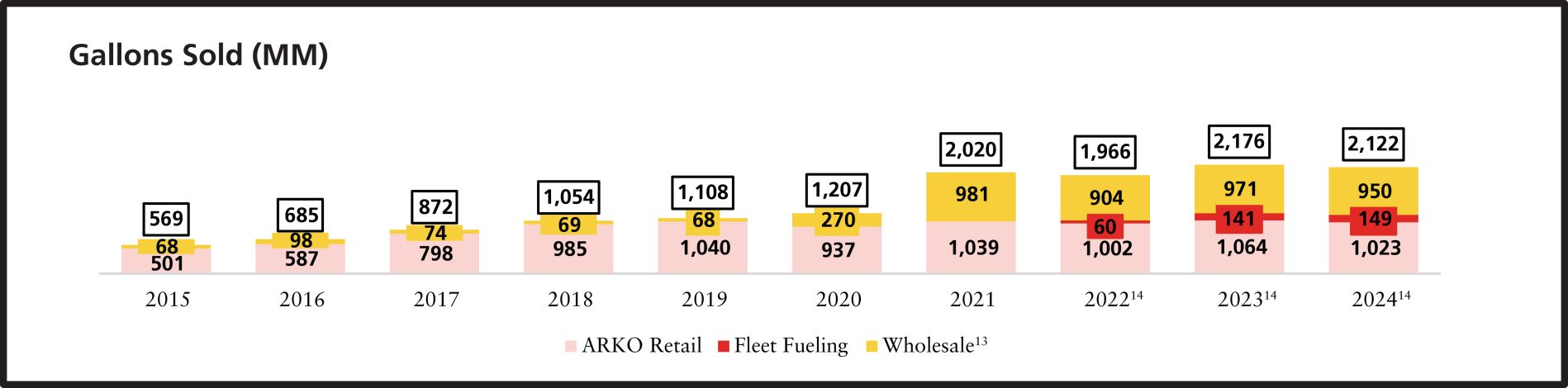

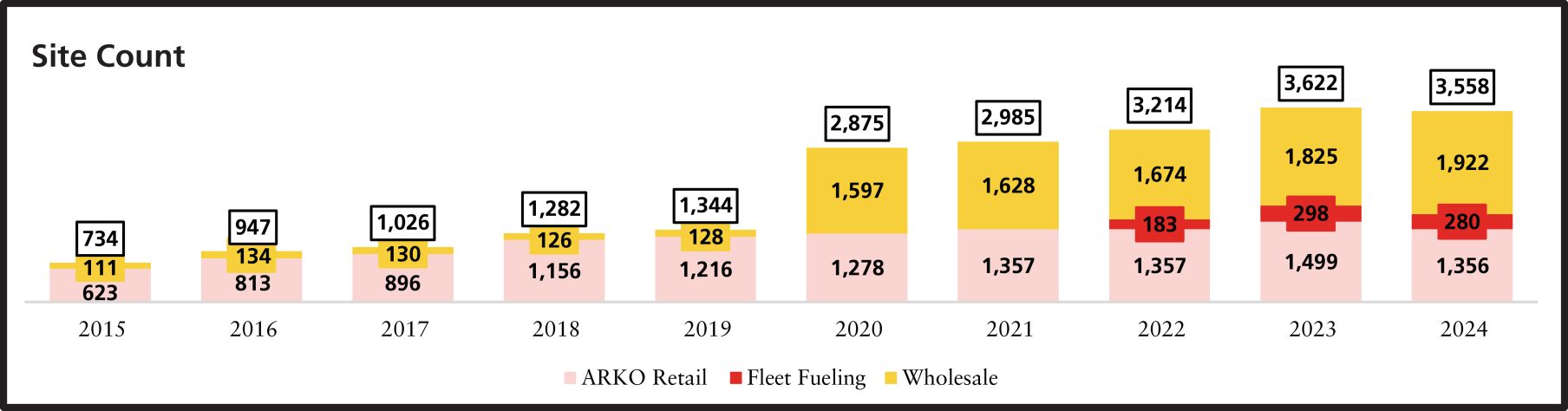

We have a proven track record of long-term, sustainable growth in gallons distributed. Between January 1, 2020 and September 30, 2025, we grew our gallons distributed or sold by a compounded annual growth rate (“CAGR”) of approximately 12%, driven primarily by the addition of 624 net new sites (inclusive of ARKO Retail Sites), bringing our total sites to 3,499 as of September 30, 2025, and our fuel margin by a CAGR of approximately 14% over the same time period.

As of September 30, 2025, our business operations included:

| • | Supplying fuel to 1,158 ARKO Retail Sites, pursuant to a long-term motor fuel distribution agreement with ARKO Parent |

| • | Supplying fuel to 2,053 gas stations operated by third-party dealers, pursuant to long-term agreements |

| • | The operation of a total of 288 proprietary and third-party unstaffed cardlock locations |

We have designed our operating model to be cost-and-capital-efficient based on the following characteristics: (i) the business requires a limited number of employees; (ii) relatively low operating costs, which generally result in high conversion of gross profit to Adjusted EBITDA1 and, similarly, an attractive margin profile; and (iii) adding wholesale and cardlock sites is not expected to require substantial incremental corporate overhead, providing an opportunity to scale efficiently. Additionally, our cost-and-capital-efficient operating model, relatively low leverage and stable and growing cash flow profile, are expected to position us to consistently convert a high level of Adjusted EBITDA1 into Discretionary Cash Flow1, enabling us to prioritize the return of capital to shareholders in the form of consistent and growing cash dividends.

| 1 | EBITDA, Adjusted EBITDA and Discretionary Cash Flow are non-GAAP measures. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Use of Non-GAAP Measures.” |

5

Table of Contents

Prospectus Summary

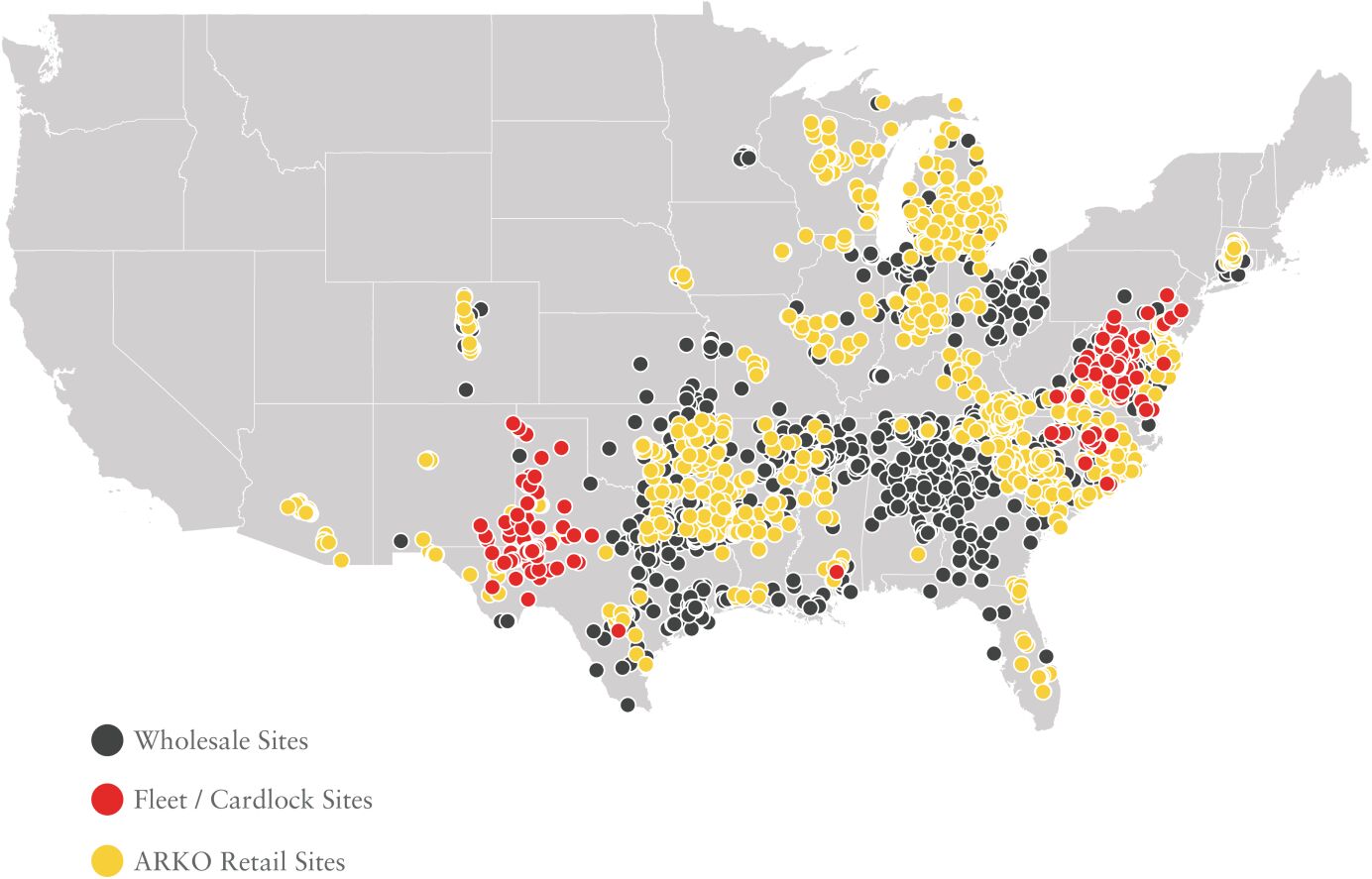

Map of ARKO Petroleum Corp.’s Wholesale, ARKO Retail and Fleet Fueling Sites2

Our Relationship with ARKO Parent

One of our principal strengths is our relationship with ARKO Parent, which operates one of the largest convenience store chains in the U.S. and is publicly listed on Nasdaq, with its common stock trading under the symbol “ARKO.” In connection with this offering, ARKO Parent will contribute all of its Wholesale and Fleet Fueling business to APC together with the supply of fuel to the ARKO Retail Sites. After the completion of this offering, ARKO Parent, indirectly through its wholly-owned subsidiary, Arko Convenience Stores, LLC (“ACS”), will own 35,000,000 shares of our Class B common stock, representing 76.9% of the economic interests in us and 94.3% of the combined voting power of our Class A common stock and Class B common stock (or 74.3% of the economic interests in us and 93.5% of the combined voting power of our Class A common stock and Class B common stock if the underwriters exercise their over-allotment option to purchase additional shares of Class A common stock in full). Upon completion of this offering, we will be a subsidiary of ARKO Parent and “controlled company” within the meaning of the rules of Nasdaq and, as a result, there may be conflicts of interest from time to time. ARKO Parent is expected to continue to own a significant controlling interest in APC following this offering and will therefore have the ability to determine all matters requiring approval by our stockholders, including the election of our directors, amendment of our governing documents, and approval of certain major corporate transactions. See “—Controlled Company Status.” ARKO Parent is a committed customer and has agreed to purchase fuel from us as part of its ongoing supply needs pursuant to the Fuel Distribution Agreement (as defined herein) to be entered into with ARKO Parent in connection with this offering. Any conflicts of interest between ARKO Parent and us will be reviewed by our Board of Directors’ Conflicts Committee (the “Conflicts Committee”). We will enter into certain contractual arrangements governing our commercial, operational and governance relationship with ARKO Parent, consisting of a Management Services Agreement, an Omnibus

| 2 | APC site location data as of September 30, 2025. |

6

Table of Contents

Prospectus Summary

Agreement, an Employee and Intercompany Matters Agreement, a Fuel Distribution Agreement, a Tax Matters Agreement, a Registration Rights Agreement and certain real estate arrangements. For a description of such agreements, see “Business—Agreements with ARKO Parent” and “Certain Relationships and Related Party Transactions.” For more information regarding our arrangements with ARKO Parent, see the sections entitled “Risk Factors—Risks Related to the Transactions and our Governance Relationship with ARKO Parent” and “Management—Board Committees—Conflicts Committee.”

ARKO Parent operates convenience stores that sell fuel products and merchandise to retail customers through more than 25 regional store brands. The vast majority of ARKO Parent-operated convenience stores sell fuel. For the year ended December 31, 2024, ARKO Parent’s retail segment generated total revenues of $5.3 billion, including $1.8 billion of in-store sales and other revenues. During that same period, ARKO Parent sold 1.1 billion gallons of branded and unbranded fuel to its retail customers. For the nine-months ended September 30, 2025, ARKO Parent’s retail segment generated total revenues of $3.4 billion, including $1.2 billion of in-store sales and other revenues. During that same period, ARKO Parent sold 704 million gallons of branded and unbranded fuel to its retail customers. We enjoy substantial purchasing power across our entire platform as a result of supplying fuel to ARKO Parent.

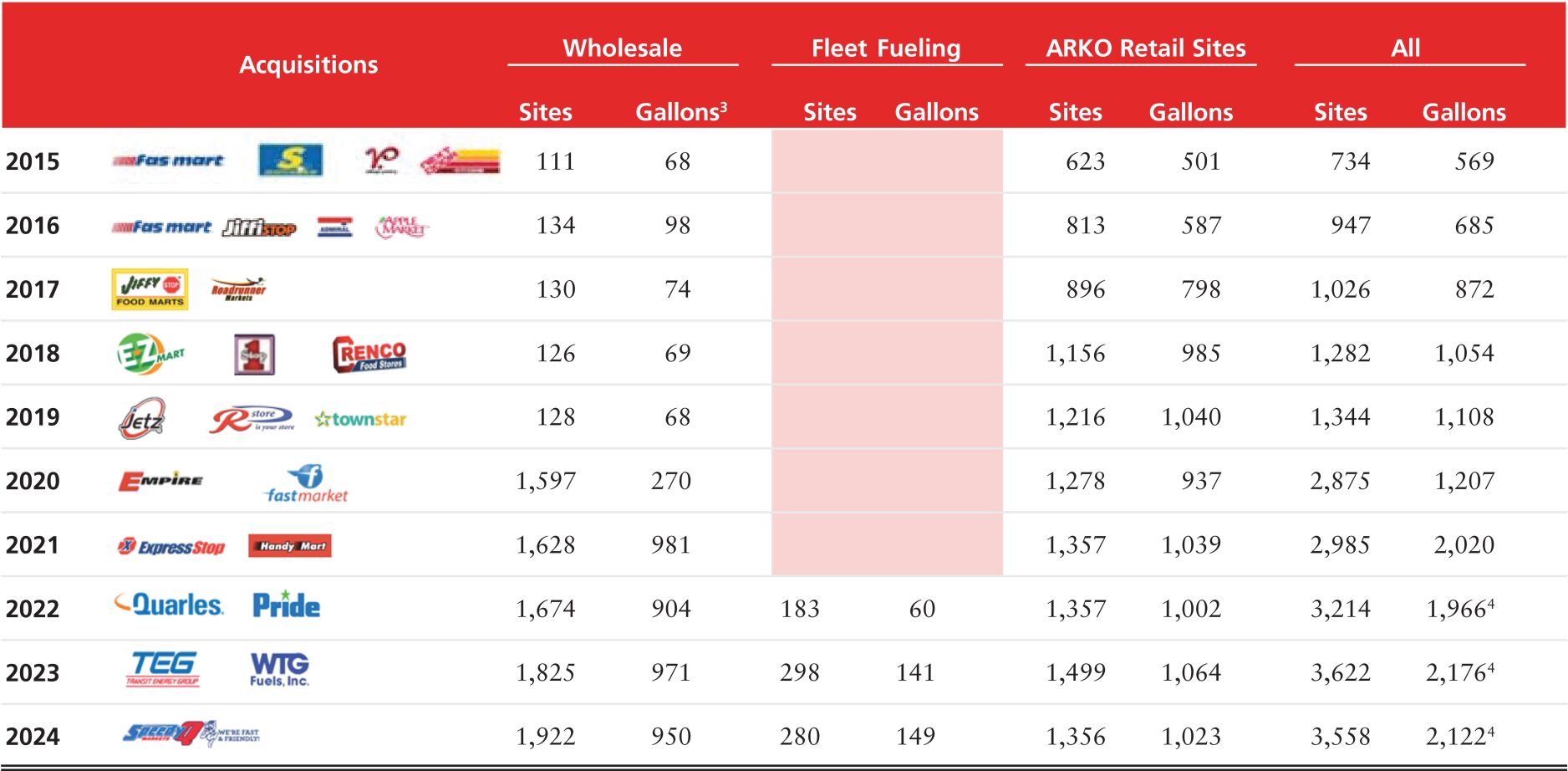

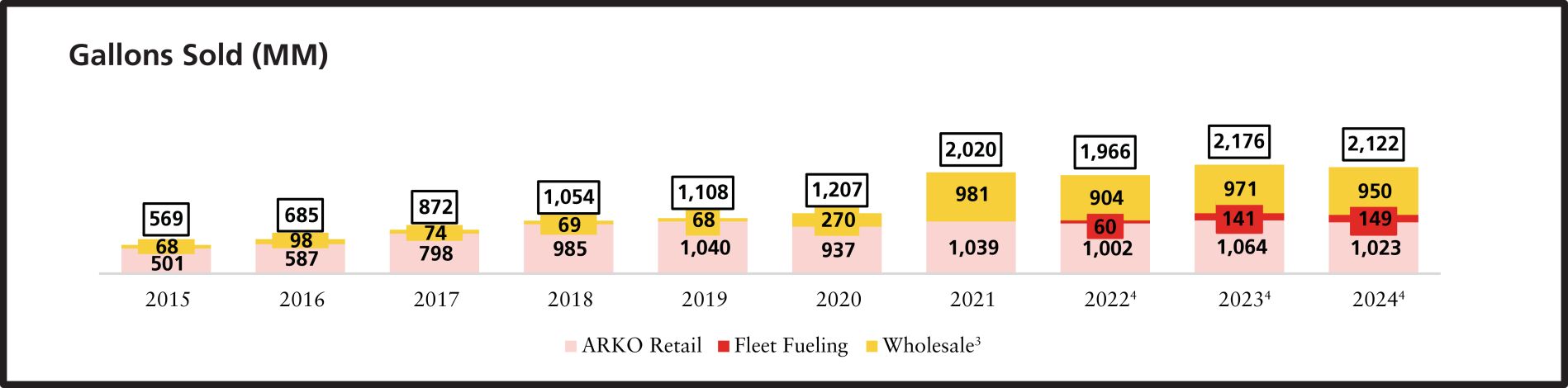

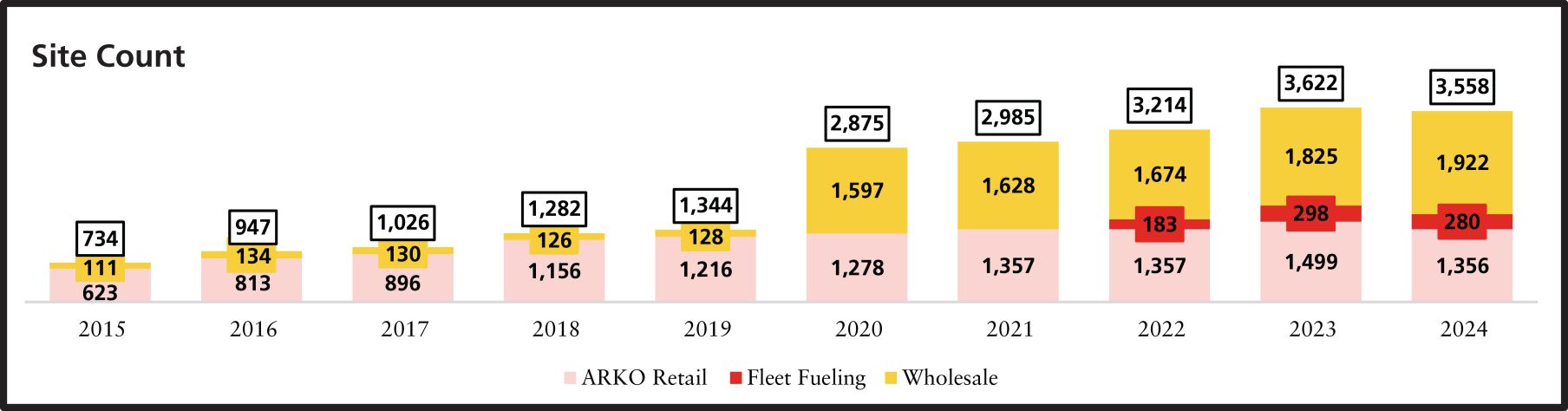

In October 2020, ARKO Parent significantly expanded its wholesale business following the acquisition of the business of Empire Petroleum Partners. Subsequently, ARKO Parent established its fleet fueling business following the acquisition of the fleet fueling division of Quarles Petroleum, incorporated in July 2022. ARKO Parent continued to grow the Wholesale and Fleet Fueling businesses through acquisitions from Transit Energy Group and WTG Fuels, respectively.

Future ARKO Retail organic growth and acquisitions benefit us by: (i) increasing our contracted gallons sold to ARKO Retail Sites and (ii) broadening the opportunity set of desirable M&A targets for us to include Wholesale and Fleet Fueling business that are part of retail companies which may be acquired by ARKO Parent, leveraging ARKO Parent’s strong history of retail growth. Aside from ARKO Retail, no single customer currently accounts for more than approximately 1.0% of gallons annually. As we grow our business going forward, we plan to diversify our customer base and decrease our concentration of fuel distributed to ARKO Retail Sites.

In the middle of 2024, ARKO Parent commenced a multi-year transformation plan that includes the conversion of a meaningful number of ARKO Retail Sites to wholesale third-party dealer sites. Our sales team successfully converted 347 ARKO Retail Sites to third-party dealer sites from the beginning of 2024 through September 30, 2025 and is focused on converting additional sites in the future. Our sales team comprises employees of ARKO Parent’s wholesale business who will become our employees. As of September 30, 2025, ARKO Parent has an aggregate of approximately 185 sites committed for future conversion which are currently under letter of intent or contract or have been converted since the end of the quarter, with a further meaningful pipeline for conversion ahead. Following the completion of this offering, ARKO Parent will continue to operate a significant retail business.

7

Table of Contents

Prospectus Summary

Note: Statistics are cumulative based on year end for its respective period. Gallon data is displayed in millions of gallons of fuel sold.

Our Lines of Business

Gallons Sold and Site Count (mm)5:

| 3 | Includes immaterial gallons sold by GPMP to third-party dealers. |

| 4 | Excludes gallons sold by our non-reportable segments. |

| 5 | In July 2022, we added the Fleet Fueling segment to our business. |

8

Table of Contents

Prospectus Summary

Wholesale Segment

Our Wholesale segment supplies fuel to gas stations operated by third-party dealers, sub-wholesalers, and bulk and spot purchasers on either a cost-plus, or consignment basis, the material terms of which are described below. For cost-plus fuel supply contracts, the dealer purchases the fuel from us, and we earn a fixed mark-up above our costs. Under consignment contracts, the Company owns the fuel product until sold to the final customer. Additionally, we generally retain any applicable prompt pay discounts and rebates we receive from our fuel suppliers. Historically, the majority of the fuel supply and consignment contracts with our dealers have been renewed at the end of their terms.

| • | Fuel supply contracts. As of September 30, 2025, we had 1,757 sites under fuel supply contracts on a cost-plus basis. Our fuel supply contracts are generally exclusive supply agreements with an initial term of 10 years. As of September 30, 2025, the volume-weighted average remaining term for our cost-plus sites was approximately 5.2 years. In addition, we supply fuel, on a cost-plus basis, to a number of additional bulk and spot customers on a non-exclusive basis. The sales price to the dealer is determined according to the terms of the relevant contract, which typically reflects our total fuel costs plus the cost of transportation, taxes and our fixed margin. These terms limit our exposure to commodity price volatility. Furthermore, we generally retain any prompt pay discounts and rebates from our fuel suppliers. Our dealers are either (i) “lessee-dealers,” if the dealer leases the convenience store from us or (ii) “open-dealers,” if the dealer owns or leases the site from another party. Property control at the lessee-dealer sites provides us with value and flexibility, along with highly stable income streams. Because we control the underlying property, our relationships with lessee-dealers are generally more durable. Of the lessee-dealer sites, we lease 340 locations and own 106 locations. |

| • | Consignment contracts. As of September 30, 2025, we had 296 sites under consignment contracts. Under these arrangements, we own the fuel until the time of sale to the final customer at the dealer site, and the gross profit from the sale of fuel is allocated between us and the dealer based on the terms of the relevant contract. There are two possible methods of allocating profit under our consignment contracts: (i) gross profit is split based on a percentage; or (ii) we pay a fixed fee per gallon to the dealer and retain the remainder of the profit. Of the sites under consignment contracts, we lease 130 locations and own 52 locations. As of September 30, 2025, the volume-weighted average remaining term for our consignment sites was approximately 4.6 years. |

Historically, the majority of growth within our Wholesale segment has been through acquisitions. We intend to continue to grow our business through strategic and accretive acquisitions of

9

Table of Contents

Prospectus Summary

wholesale distribution businesses both within our existing area of operations and in new geographic areas. Our experienced M&A team continually evaluates attractive, synergistic opportunities. Our scale and the experience of our management team gives us the flexibility to pursue a wide range of opportunities from bolt-on acquisitions to large-scale transactions. The wholesale distribution industry is fragmented, with a majority of wholesale fuel distributors operating on a smaller scale. In recent years there has been substantial consolidation involving such smaller fuel distributors, which we expect will continue. We believe there is a considerable opportunity for us to be a driver of that consolidation in our industry.

In addition to growth through acquisitions and obtaining new dealers through our internal sales efforts, we expect to continue to grow through the conversion of ARKO Retail Sites under ARKO Parent’s multi-year transformation plan. During the nine months ended September 30, 2025, our Wholesale segment grew by 194 sites through the conversion of ARKO Retail Sites to third-party dealer sites as part of ARKO Parent’s multi-year transformation plan.

Key Wholesale segment highlights:

| • | Historically stable fuel margins |

| • | Wholesale customers primarily operate under long-term, exclusive contracts |

| • | Historically stable cash flows and limited commodity price risk |

| • | The wholesale market is fragmented, and we believe ripe with potentially accretive acquisition opportunities that can be integrated by APC’s experienced M&A team |

| • | Benefits from our economy of scale and relationships with all the major oil companies |

| • | Limited ongoing maintenance capital expenditures have resulted in high conversion of EBITDA6 to Discretionary Cash Flow6 |

As of September 30, 2025, the Wholesale segment supplied fuel to 2,053 sites. For the year ended December 31, 2024, the Wholesale segment sold 949 million gallons of fuel, generating revenues of $2.8 billion, and fuel contribution of $90 million. For the nine-month period ended September 30, 2025, the Wholesale segment sold 740 million gallons of fuel, generating revenues of $2.09 billion, and fuel contribution of $70.5 million.

Fleet Fueling Segment

The Fleet Fueling segment includes the operation of proprietary and third-party cardlock locations (unstaffed fueling locations) that sell fuel (primarily diesel) to commercial fleets (including light industrial trucks and commercial vehicles) and municipal entities. The Fleet Fueling segment generates additional revenue through commissions from the sale of fuel at third-party locations to customers using our proprietary fuel cards, which are accepted at a nationwide network of more than 320,000 retail and private fueling sites, truck stops, maintenance providers and service locations.

We believe we are a leading national cardlock operator, and we have a strong presence in the East Coast, West Texas and New Mexico. Our cardlock sites are strategically located in high-traffic corridors and service a diverse base of commercial customers across multiple industries.

| 6 | EBITDA and Discretionary Cash Flow are non-GAAP measures. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Use of Non-GAAP Measures.” |

10

Table of Contents

Prospectus Summary

Key Fleet Fueling segment highlights:

| • | As of September 30, 2025, diesel fuel accounted for approximately 80% of our fleet fuel sales, which historically has generated more attractive margins relative to gasoline |

| • | On-site labor is unnecessary to run cardlocks, creating attractive site level economics |

| • | Sites present efficient site design, optimal location selection with a built-in customer base due to a high concentration of commercial businesses |

| • | New cardlock locations can offer high return, capital-efficient organic growth |

| • | Third-party cardlocks generate revenue, and we expect that there is room to grow the number of third-party cardlocks we supply through territorial expansion and moderate pricing power |

| • | The fleet fueling market is fragmented and we believe ripe with potentially accretive acquisition opportunities that can be integrated by APC’s experienced M&A team |

As of September 30, 2025, the Fleet Fueling segment operated a total of 288 sites. For the year ended December 31, 2024, the Fleet Fueling segment sold 149 million gallons of fuel, generating revenues of $525 million, and fuel contribution of $64 million. For the nine-month period ended September 30, 2025, the Fleet Fueling segment sold 108 million gallons of fuel, generating revenues of $366 million, and fuel contribution of $49.8 million.

GPMP segment

Our GPMP segment includes the supply of fuel to substantially all of the ARKO Retail Sites at our cost of fuel (including taxes and transportation) plus a fixed margin (5.0 cents per gallon prior to January 1, 2026 and 6.0 cents per gallon thereafter) with ARKO Parent receiving any prompt pay discounts and rebates. The sales to ARKO Retail Sites, similar to our Wholesale cost-plus arrangements, limit our exposure to commodity price volatility. In addition, our GPMP segment charges a fixed fee (5.0 cents per gallon prior to January 1, 2026 and 6.0 cents per gallon thereafter) to certain of the ARKO Retail Sites that are not supplied by us. Our GPMP segment also includes inter-segment transactions for the sale of fuel to substantially all of our Wholesale locations at our cost of fuel (including taxes and transportation) plus a fixed margin (5.0 cents per gallon prior to January 1, 2026 and 6.0 cents per gallon thereafter) and charges a fixed fee (5.0 cents per gallon prior to January 1, 2026 and 6.0 cents per gallon thereafter) primarily to fleet fueling locations that are not supplied by our GPMP segment. All inter-segment transactions are eliminated in the combined financial statements included in this prospectus.

As of September 30, 2025, the GPMP segment supplied fuel to 1,158 ARKO Retail Sites. For the year ended December 31, 2024, the GPMP segment sold 1,023 million gallons of fuel to ARKO Retail Sites, generating from ARKO Retail Sites revenues of $3.0 billion and fuel contribution of $51 million. For the nine-month period ended September 30, 2025, the GPMP segment sold 661 million gallons of fuel to ARKO Retail Sites, generating from ARKO Retail Sites revenues of $1.79 billion and fuel contribution of $33 million.

11

Table of Contents

Prospectus Summary

Our Business Strategies

Our primary business objective is to maintain and sustainably grow cash flows and to make increasing cash distributions to our stockholders over time by increasing gallons sold. We intend to accomplish these objectives by executing the following strategies:

| • | Focus on Stable, Fee-based Activities that Provide Long-term Value for our Stockholders by: |

| • | Maintaining cash flow stability. We are committed to maintaining cash flow stability by continuing to enter into cost plus, long-term supply contracts, which generally minimize commodity price risk due to our predominantly cost-plus model. |

| • | Continuing to leverage our relationships with fuel suppliers. We intend to continue to leverage our strong relationships with major fuel suppliers to provide attractive fuel pricing to our customers, acquire additional wholesale distribution contracts with additional rebates. |

| • | Sustainably growing cash available for dividends to stockholders over time. Our primary goal is to maximize investor returns through cash distributions by continuing to grow fuel distribution volumes and maintaining a conservatively capitalized balance sheet with ample financial flexibility. |

| • | Leverage Our Relationship with ARKO Parent to Maintain and Grow Stable Cash Flows by: |

| • | Increasing our fuel distribution volumes by growing volumes of fuel sold at both existing and new-to-industry ARKO Retail Sites. ARKO Parent is a committed customer and has agreed to continue purchasing fuel from us as part of its ongoing supply needs through long-term contractual arrangements with us. ARKO Parent has recently begun investing its capital toward strategic sub-segments of its retail stores and new-to-industry sites, with a goal of increasing traffic and fuel gallons sold. |

| • | Increasing our fuel distribution volumes through supplying fuel to new sites acquired by ARKO Parent. ARKO Parent has a proven track record of acquiring and integrating sizeable packages of convenience stores, and we anticipate future ARKO Parent acquisitions will provide APC with an opportunity to capitalize on additional fuel volumes sold through new ARKO Retail sites. |

| • | Pursuing strategic acquisition opportunities with ARKO Parent. Given the ownership fragmentation across the fuel distribution and retail convenience store industries, we believe that there is considerable opportunity for us to capitalize on industry consolidation. We intend to capitalize on the relationship between our business and ARKO Parent’s complementary retail business by jointly pursuing acquisition opportunities. Acquisitions exclusive to ARKO Retail will still offer the opportunity for us to concurrently grow through the purchase of fuel distribution rights. |

| • | Expand Our Third-Party Wholesale Distribution and Fleet Fueling Businesses by: |

| • | Increasing our wholesale dealer network through recruitment of new dealers. We plan to continue to organically grow our Wholesale business by increasing the number of dealer locations. We benefit from a large-scale sales force of approximately 50 dedicated representatives actively pursuing new contracts and customers as an ordinary course of business expansion. We also offer the option for our dealers to participate in our Preferred Vendor Program (“PVP”), which allows our dealers to receive the benefit of more competitive group pricing from non-fuel vendors while also providing us rebates on purchases from selected vendors and making such dealer relationships stickier. |

12

Table of Contents

Prospectus Summary

| • | Growing our Fleet Fueling business by increasing fuel volumes with existing commercial accounts and municipalities and growing our network of accounts. We plan to grow our high-margin Fleet Fueling segment through investing in targeted equipment upgrades and branding enhancements to drive volume growth at existing sites. Additionally, our in-house sales team will be focused on organically growing existing and new accounts at our existing cardlocks. |

| • | Expand our Fleet Fueling footprint by building new locations. We intend to leverage our experienced management team to identify attractive geographic markets for new-to-industry site development in both existing and new markets. |

| • | Executing attractive and accretive acquisitions and optimizing assets through effective integration. We have a strong track record of successfully acquiring and integrating smaller distributors and fleet fueling businesses that have expanded our market presence, operational scale and increased fuel volumes with fuel suppliers, with minimal additional back-office costs. Our experienced M&A team is continually evaluating opportunities, leveraging a breadth of industry relationships, our strong reputation, and a long track record of success in both wholesale and fleet fueling M&A. Our scale and the experience of our management team gives us the flexibility to pursue a wide range of acquisition opportunities from small bolt-on acquisitions to large-scale transactions. We believe acquiring incremental dealer and cardlock locations may enhance our scale benefits by lowering fuel purchasing costs and creating a business with an attractive margin profile. |

| • | Maintain a Conservative Capital Structure with Enhanced Financial Flexibility by: |

| • | Pursuing a conservatively capitalized balance sheet with disciplined financial policy. We plan to maintain a conservative balance sheet that provides ample liquidity and financial flexibility. Based on our revolving borrowing capacity under our Capital One Line of Credit (as defined below) and cash on hand, we had liquidity of $444 million as of December 31, 2024, consisting of approximately $25 million of cash and cash equivalents as of December 31, 2024, and approximately $418.7 million of availability under our Capital One Line of Credit. As of September 30, 2025, we had indebtedness of $389 million and $33 million cash on hand, resulting in a ratio of total debt, net to net income for the last twelve months of 12.1x and a Ratio of Net Debt to Adjusted EBITDA7 for the last twelve months of 3.4x. We are targeting what we believe to be a peer leading Ratio of Net Debt to Adjusted EBITDA of less than 2.5x immediately after giving effect to this offering and the application of the proceeds from this offering as described in “Use of Proceeds.” Based on our revolving borrowing capacity under our Capital One Line of Credit and cash on hand, we had liquidity of $451.7 million as of September 30, 2025, consisting of approximately $33.0 million of cash and cash equivalents and $418.7 million of unused availability under our $800 million Capital One Line of Credit. |

Our Competitive Strengths

We believe that the following strengths will allow us to successfully execute our business strategies:

| • | Experienced management team with an extensive track record of growth. We believe our management team’s significant industry experience is a differentiated competitive advantage. The members of our management team have over 100 years of combined experience in the convenience store and fuel distribution industry. |

| 7 | Net Debt, Adjusted EBITDA and Ratio of Net Debt to Adjusted EBITDA are non-GAAP measures. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Use of Non-GAAP Measures.” |

13

Table of Contents

Prospectus Summary

| • | Relationship with ARKO Parent. One of our key strengths is our relationship with ARKO Parent, which provides us with valuable scale advantages, growth opportunities, and a growing customer network, including 2.39 million enrolled members in its fas REWARDS® loyalty program, which is available in all ARKO Retail Sites and offers members in store exclusive promotional pricing, in-app member only deals and the ability to earn points that can be redeemed for either fuel or merchandise savings. We believe that ARKO Parent will be incentivized to grow our business because of its significant economic interest in us as our majority stockholder. Moreover, we believe that the relationship between our wholesale business and ARKO Parent’s complementary retail business fosters a mutually beneficial commercial relationship that allows us and ARKO Parent to benefit from our combined economies of scale and purchasing power. |

| • | Significantly scaled operations. We are one of the largest wholesale fuel distributors in the U.S. and believe we are uniquely positioned to gain market share in a highly fragmented market. We are also able to leverage our scale to enhance efficiencies, including capturing competitive pricing terms and offering multiple fuel branding options for our customers through our strong relationships with our major fuel supply partners such as: BP, ExxonMobil, Marathon, Motiva, Shell, and Valero. We believe that the variety of branded and unbranded motor fuel that we distribute is a key competitive advantage over many other wholesale fuel distributors. As an independent wholesale distributor with strong relationships with a diverse group of major oil companies, we are able to tailor our distribution of specific brands to dealers in geographic regions with demonstrated brand preferences. |

| • | Ability to source, integrate and optimize acquisitions. Our strong industry relationships and ability to source and execute accretive acquisitions have allowed us to identify and negotiate transactions on attractive terms, which we expect to continue. Furthermore, we have successfully extracted synergies after integration by reducing overhead costs and leveraging our economies of scale. |

| • | Conservatively capitalized balance sheet and strong liquidity profile. We have a strong and conservative financial position that allows us to effectively allocate capital, organically grow our volume of fuel distributed, and pursue opportunistic and accretive acquisitions to support our primary objective of providing long-term value to our stockholders via the maximization of cash distributions. |

Summary of Conflicts of Interest with ARKO Parent

While our relationship with ARKO Parent is a significant strength, it is also a source of potential conflicts. Potential conflicts may arise between ARKO Retail and us in a number of areas relating to our strategic relationship, including but not limited to the nature, quality, and pricing of services ARKO Parent has agreed to provide us, and any new commercial arrangements between ARKO Parent and us in the future. The resolution of any potential conflicts or disputes between ARKO Parent and us may be less favorable to us than the resolution we might achieve if we were dealing with an unaffiliated third party. We expect to address any such conflicts by requiring specific matters that our Board of Directors believes may involve conflicts of interest to be reviewed and approved by our independent Conflicts Committee. Additionally, we expect a majority of our directors will also be directors of ARKO Parent, and our amended and restated certificate of incorporation will provide that we renounce any interests or expectancy in corporate opportunities which become known to (i) any of our directors, officers, managers, employees or agents who also are directors, officers, employees, agents or affiliates of ARKO Parent or its affiliates (except that we and our subsidiaries will not be deemed affiliates of ARKO Parent or its affiliates for the

14

Table of Contents

Prospectus Summary

purposes of the provision) or (ii) ARKO Parent or its affiliates. For a more detailed description of such conflicts of interest and the related risks, see “Risk Factors—Risks Related to the Transactions and our Governance Relationship with ARKO Parent,” “Certain Relationships and Related Party Transactions” and “Description of Capital Stock—Conflicts of Interest.”

The Transactions

Prior to this offering, ARKO Parent will transfer certain real estate and equipment assets to the Contributed Businesses. In connection with the closing of this offering, we and ARKO Parent will complete a series of transactions whereby ARKO Parent will (i) transfer certain additional real estate and equipment assets to the Contributed Businesses, along with assigning, leasing or subleasing the leasehold interest in certain properties, (ii) contribute all of the issued and outstanding equity interests in the Contributed Businesses to us such that the Contributed Businesses will be our wholly owned subsidiaries, (iii) enter into, or amend, various agreements with us, including agreements pursuant to which our GPMP segment will be the exclusive supplier of motor fuel to ARKO Retail Sites (see “Business”), (iv) amend and restate our certificate of incorporation to, among other things, provide for Class A common stock and Class B common stock, with the holders of our Class A common stock entitled to one vote per share and the holders of our Class B common stock entitled to five votes per share, in each case on all matters submitted to a vote of our stockholders, and provide that shares of Class B common stock may only be owned by ARKO Parent and its affiliates (other than us), and (v) we will issue a wholly owned subsidiary of ARKO Parent 35,000,000 shares of Class B common stock, representing 76.9% of the economic interests in us and 94.3% of the combined voting power of our Class A common stock and Class B common stock (or 74.3% of the economic interests in us and 93.5% of the combined voting power of our Class A common stock and Class B common stock if the underwriters exercise their over-allotment option to purchase additional shares of Class A common stock in full). Additionally, in connection with such transactions, certain of the ARKO Parent subsidiaries contributed to us will transfer to ARKO Parent certain real estate assets not related to the ongoing operations of the Contributed Businesses and we will enter into certain subleases, as the sublessee, and master leases, as cotenant or a sublessee, with ARKO Parent for the sites on which we operate.

We collectively refer to the foregoing transactions, this offering, as the “Transactions.”

Immediately following the completion of the Transactions, ARKO Petroleum Corp. will be a holding company and its principal assets will be ARKO Parent’s Wholesale and Fleet Fueling businesses and the supply of fuel to ARKO Retail Sites.

Following the Transactions, ARKO Parent will hold 94.3% of the total voting power of both classes of our common stock outstanding after this offering (or 93.5% of the total voting power of both classes of our common stock if the underwriters exercise their over-allotment option to purchase additional shares of Class A common stock in full) and will therefore have the ability to determine all matters requiring approval by our stockholders, including the election of our directors, amendment of our governing documents, and approval of certain major corporate transactions. See “—Controlled Company Status.”

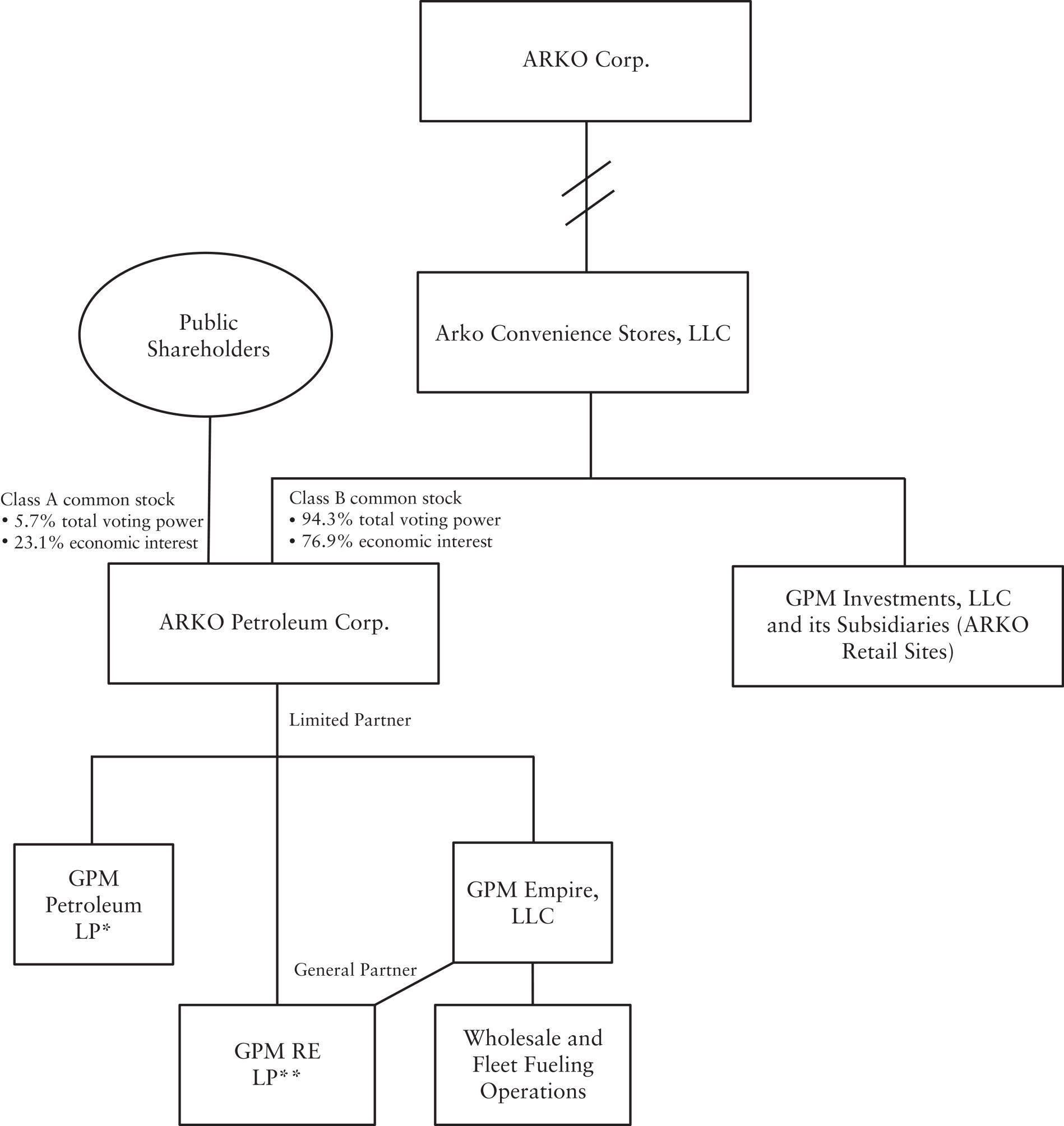

Corporate Structure

The following diagram sets forth a simplified view of our corporate structure after giving effect to the completion of the Transactions, including this offering. This chart is for illustrative purposes only and does not represent all legal entities affiliated with ARKO Petroleum.

15

Table of Contents

Prospectus Summary

| * | GPM Petroleum LP, its general partner and operating subsidiary are not guarantors under ARKO Parent’s Senior Notes. See “Description of Certain Indebtedness” for additional information on our and ARKO Parent’s debt instruments and the parties thereto. |

| ** | GPM RE LP, holds fee simple interest in most of our owned real estate. |

16

Table of Contents

Prospectus Summary

Corporate Information

ARKO Petroleum is a Delaware corporation and was incorporated on July 2, 2025. ARKO Petroleum’s principal executive offices are located at 8565 Magellan Parkway, Suite 400, Richmond, Virginia 23227-1150 and its phone number is (804) 730-1568. ARKO Petroleum’s website can be found at www.arkopetroleum.com. The information contained on or accessible through ARKO Petroleum’s website is not incorporated into, and does not form a part of, this prospectus.

Our Industry

The U.S. fuel distribution industry is an advantaged industry for multiple reasons, including the resiliency of fossil fuel demand across economic cycles, the insulation from commodity fluctuations via an ability to pass cost increases through to consumers, the varied and diverse customer use cases, the contractual nature of customer contracts and the high-level of fragmentation in the industry. Our position in the industry is bolstered by our relationship with ARKO Parent, as well as our substantial scale and number of customers.

The wholesale motor fuel industry consists of sales of branded and unbranded gasoline and on-highway diesel to retail gas station operators and other wholesale distributors. We play an important role in the energy value chain as we provide smaller fueling station operators with access to major oil companies and independent refining companies. In many cases, these operators gain access to fuel products from major oil company branded fuel and associated imaging programs (branded fuel canopies, fueling equipment and loyalty programs), which enable them to compete more effectively with larger chains. As an alternative, independent station operators may choose to create their own fuel brand offering, in which case we are likely able to supply them with fuel products at lower prices than they would otherwise be able to obtain on their own.

In general, the price of motor fuels is influenced by crude oil prices, refining and transportation costs, and other factors, such as certain regulations and taxes, which vary from state to state. Wholesale distributors purchase branded and unbranded motor fuels from integrated oil companies and refiners and take delivery of the purchased motor fuel at a distribution terminal. The price at which a wholesale distributor generally purchases motor fuel is referred to as the “rack” price, which includes the seller’s profit on the motor fuel. While certain geopolitical events, inclement weather and other factors can quickly disrupt the supply and price of crude oil or refined petroleum products, the impact on wholesale motor fuel prices may be delayed by several days or weeks. We sell motor fuels to our customers at prices that represent our cost of motor fuels plus a profit margin, helping to insulate us from commodity price risk per gallon.

The U.S. wholesale motor fuel distribution industry is intensely competitive. We compete with other fuel resellers and oil companies that market fuel directly to petroleum distributors and retailers. In the Fleet Fueling segment, we also compete against onsite delivered fuel companies; however, we believe that our large cardlock network and fleet fueling cards provide a competitive advantage. We compete, among other things, on the basis of price, service, and reliability. Today, our standing as a top ten independent fuel distributor by volume in the U.S. enables us to obtain attractive pricing and terms from fuel suppliers and thereby confers a pricing advantage as compared to smaller competitors. In addition, our scale, sophistication, access to numerous suppliers and supply points, as well as our robust energy logistics infrastructure ensure that we have

17

Table of Contents

Prospectus Summary

competitive access to supply in periods of disruption, enhancing our ability to serve as a reliable supply partner to our customers.

The U.S. fuel distribution industry is highly fragmented, characterized by a large number of relatively small, independently owned and operated local distributors, which provides us with potentially attractive acquisition opportunities as well as a competitive advantage due to our scale. According to First Research, there are approximately 6,700 domestic wholesale fuel distributors, reflecting the fragmented nature of our industry. Additionally, the largest distributor has only an 8% market share. As a historically active acquiror of retail and wholesale fuel distributors, our M&A sourcing and integration capabilities serve as a point of strength as we observe an industry will have ample, highly strategic acquisition targets.

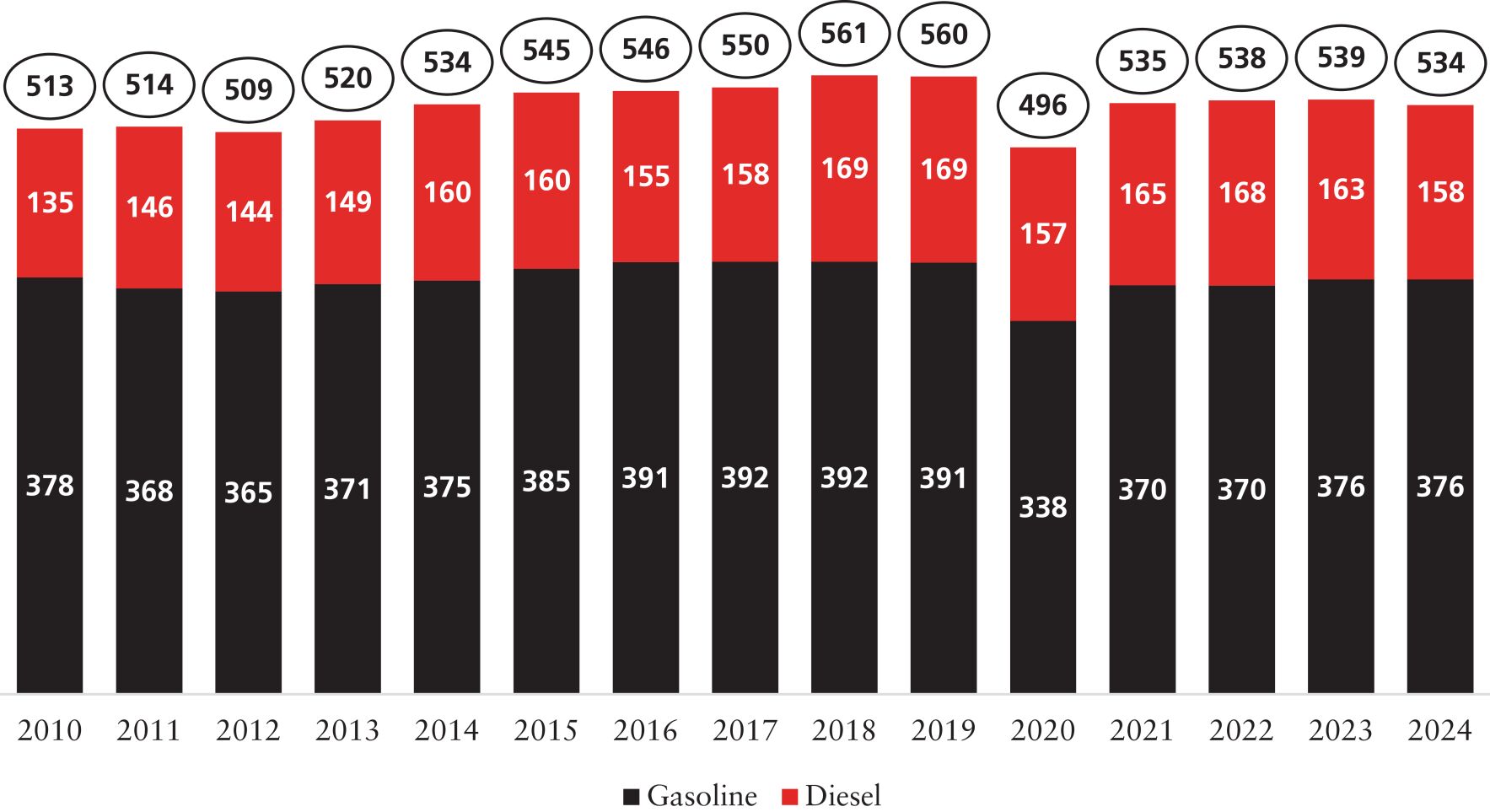

U.S. consumption of gasoline and distillate fuels has shown long term stability. In 2024, 194.8 billion gallons of gasoline and diesel fuel were supplied in the U.S. Excluding COVID-19 effects in 2020, volumes have remained between 8.7 to 9.3 million barrels per day of gasoline8 and 3.7 to 4.2 million barrels per day of distillate fuels9 since 2010, according to the U.S. Energy Information Administration (“EIA”). Moreover, the 2024 aggregate consumption returned to 94.4% of its pre-COVID peak in 2018, despite lingering work-from-home trends, improving vehicle fuel efficiency, and growing electric vehicle (“EV”) sales. Internal combustion engines continue to comprise the vast majority of vehicles on the road and new vehicles sold, with EVs projected to hold just a 26% share of vehicles on the road by 2035.10 Fueling stations have demonstrated the adaptability to evolve with consumer preferences and serve both traditional combustion engines and other types, including EVs as well as hybrids. Within this changing landscape, there is significant whitespace for growth, particularly for companies with an established market presence, proven adaptability to market demands, and operational scale.

| 8 | EIA. U.S. Product Supplied of Finished Motor Gasoline (Thousand Barrels per Day). Sourcekey: MGFEXUS2 |

| 9 | EIA. U.S. Product Supplied of Distillate Fuel Oil (Thousand Barrels per Day). Sourcekey: MDIUPUS2 |

| 10 | Edison Electric Institute. Electric Vehicle Sales and the Charging Infrastructure Required Through 2035 Report. October 2, 2024. |

18

Table of Contents

Prospectus Summary

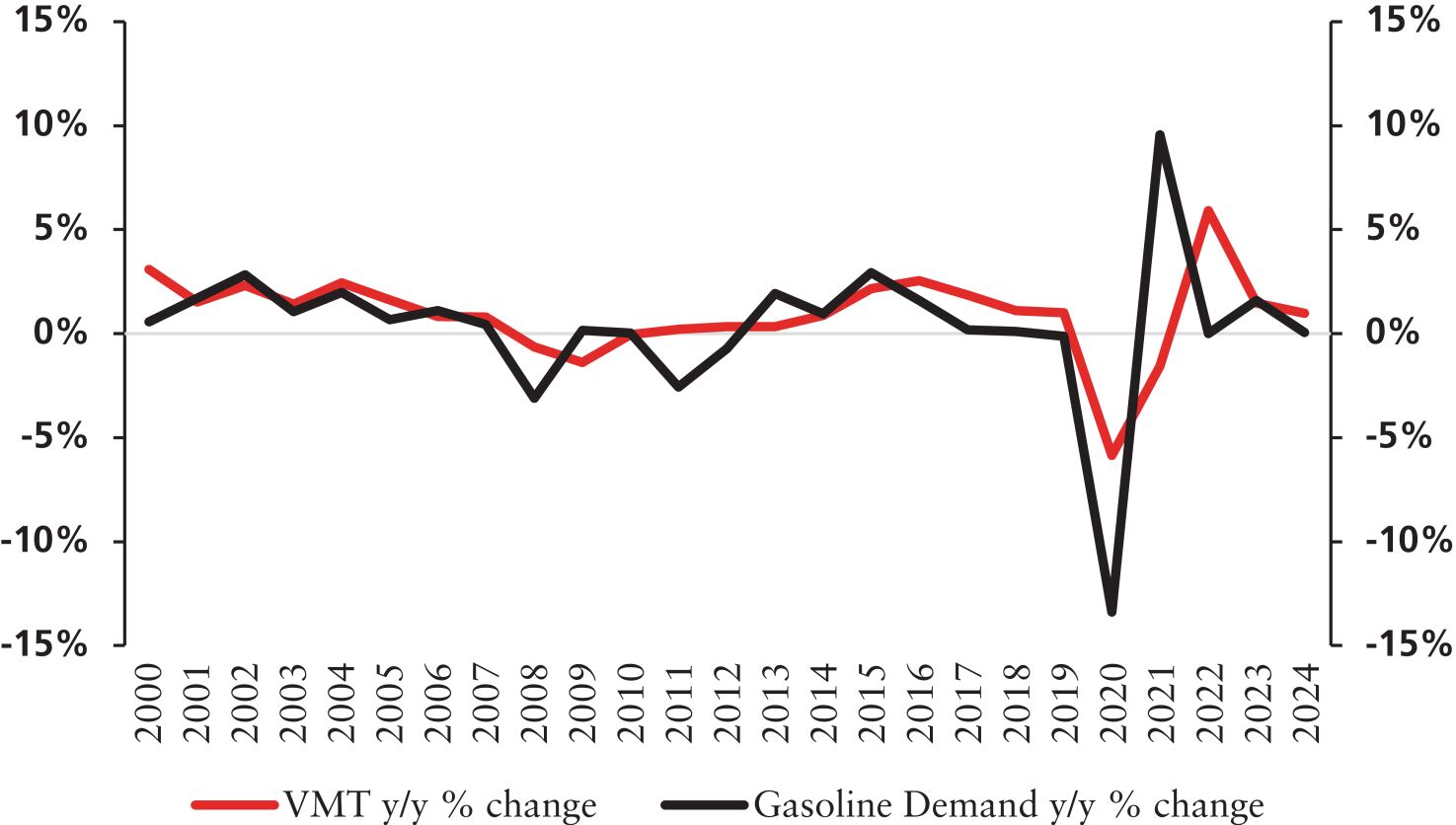

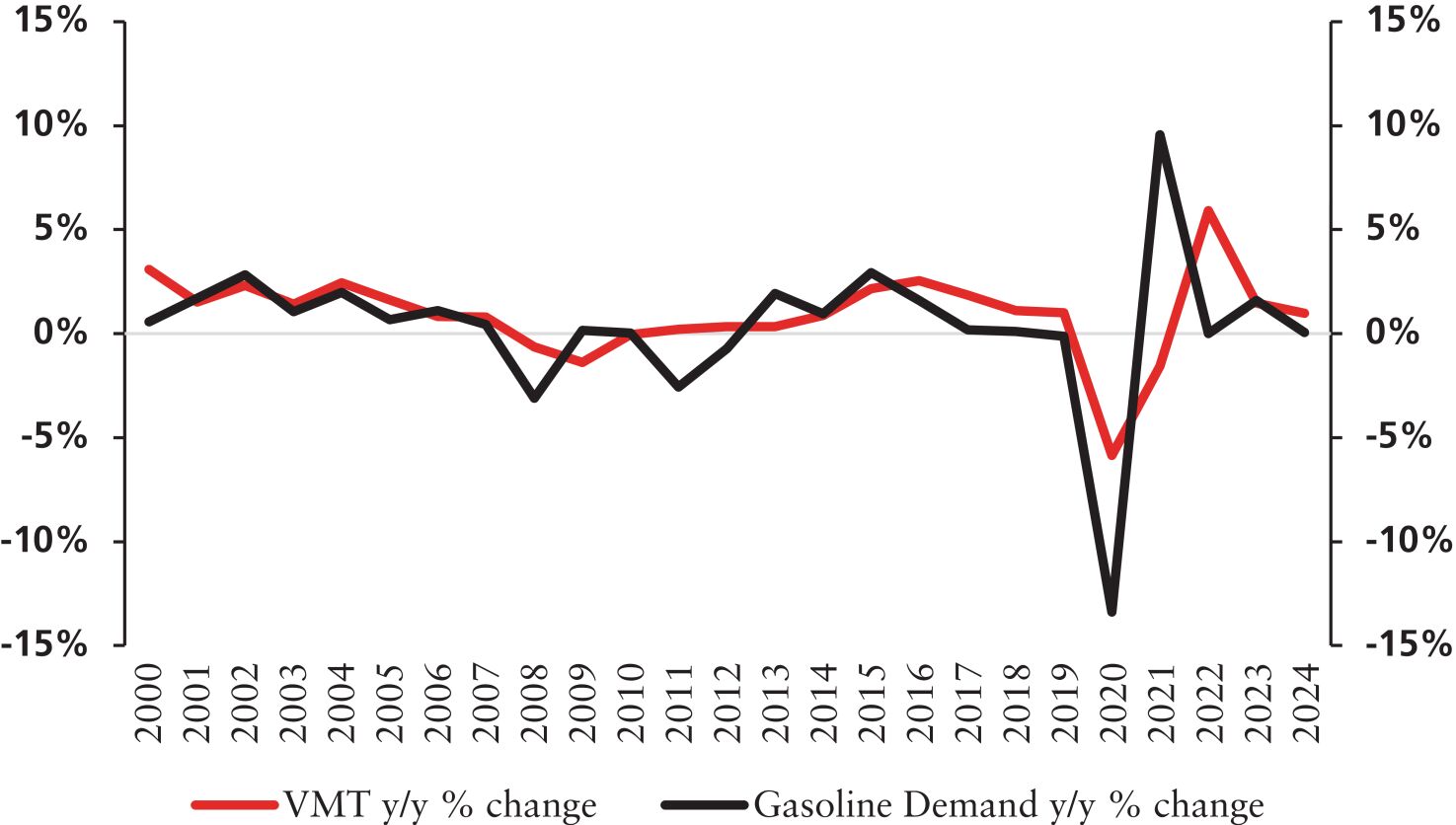

Change in Vehicle Miles Traveled (VMT) vs. Gasoline Demand YoY

Source: FRED & EIA.

Total U.S. product supplied of finished motor gasoline has remained stable for years. Additionally, annual vehicle miles traveled in the U.S. has experienced steady growth, reflecting continued reliance on personal and commercial transportation. Motor gasoline is expected to remain a critical source over the next 20+ years, bolstered by recent shifts in the automotive landscape. Major manufacturers are scaling back previously announced electric vehicle initiatives as internal combustion engine vehicles are recapturing favor among consumers. Meanwhile, the total U.S. car parc has increased by over 70 million since 2000. Within this landscape, there is significant whitespace for growth, particularly for companies with strong market positioning and operational scale, further supporting sustained fuel demand. We are well-positioned within this environment with exposure to key growth markets across the country.

19

Table of Contents

Prospectus Summary

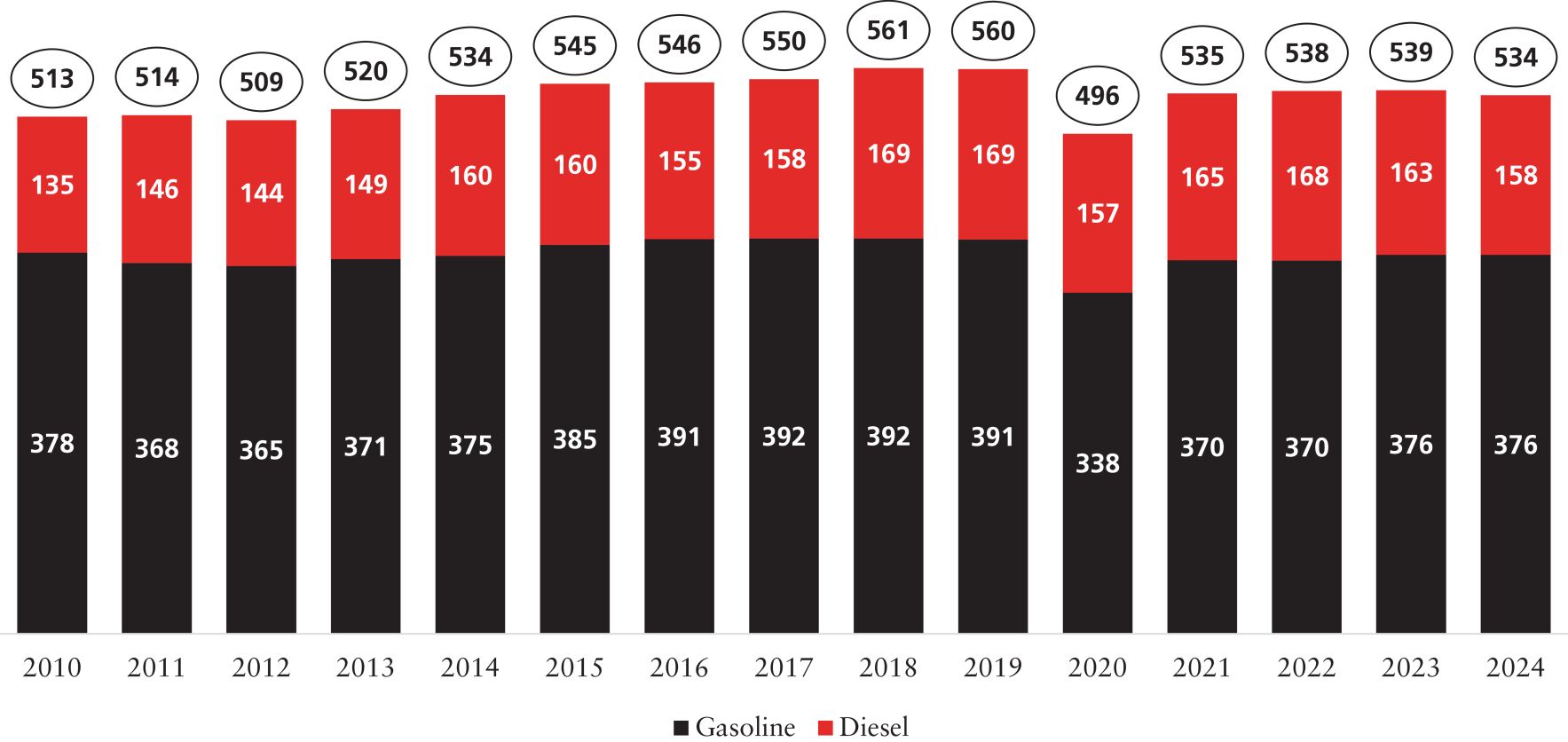

Gasoline and Diesel Supply (Millions of Gallons/Day)

Source: EIA.

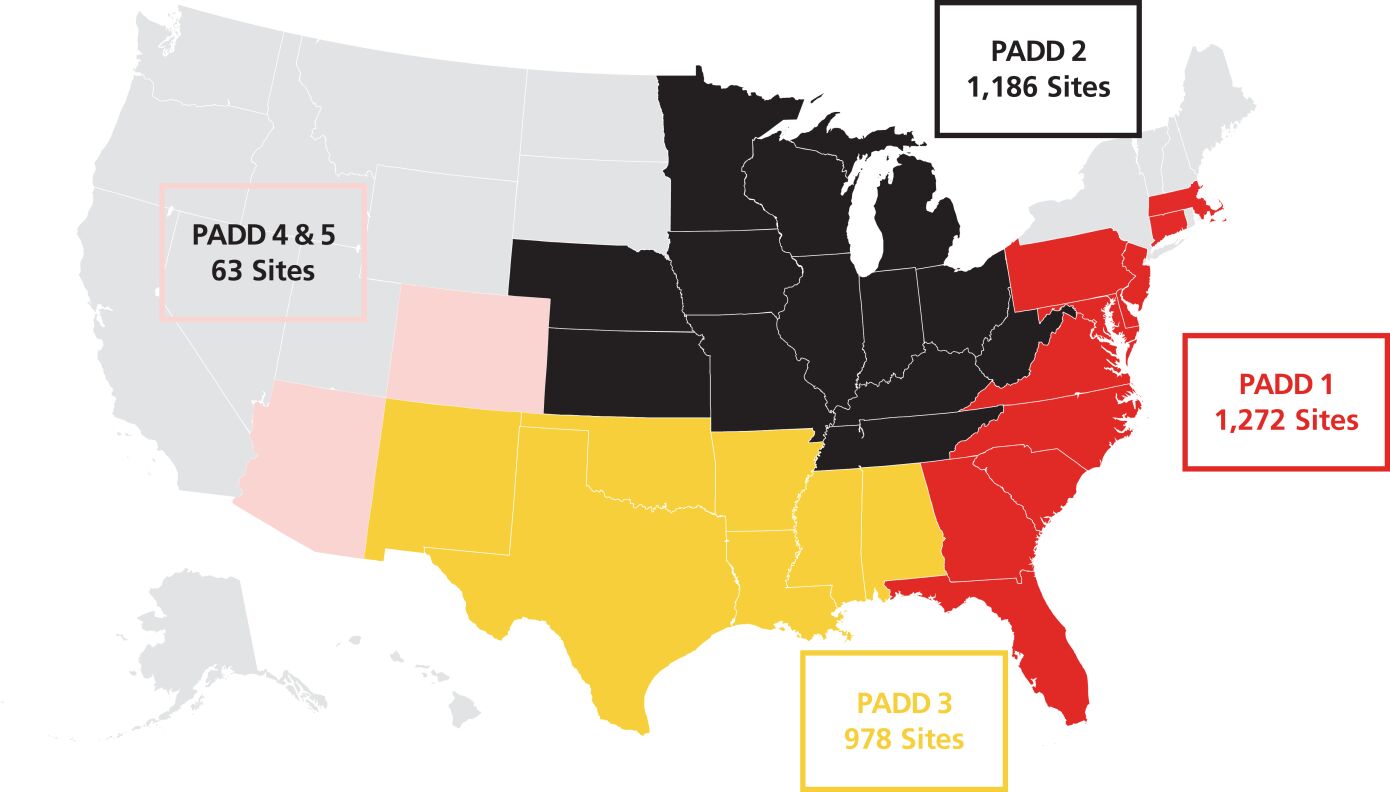

As shown in the map below, the United States is divided into five Petroleum Administration Defense Districts or “PADDs.” APC’s suppliers and customers are mostly located in PADD 1 (East Coast), 2 (Midwest), and 3 (Gulf Coast). PADD 1 consists of 7 operating refineries that can handle 0.9MMbpd of crude oil and represent 35% of total U.S. gasoline consumption. PADD 2 consists of 25 operating refineries that can handle 4.2MMbpd of crude oil and represent 29% of total U.S. gasoline consumption. PADD 3 consists of 59 operating refineries that can handle 10.1MMbpd of crude oil and represent 16% of total U.S. gasoline consumption. According to the EIA, the U.S. consumes 20.3 million barrels of refined petroleum products per day, with 8.9 million being gasoline.

20

Table of Contents

Prospectus Summary

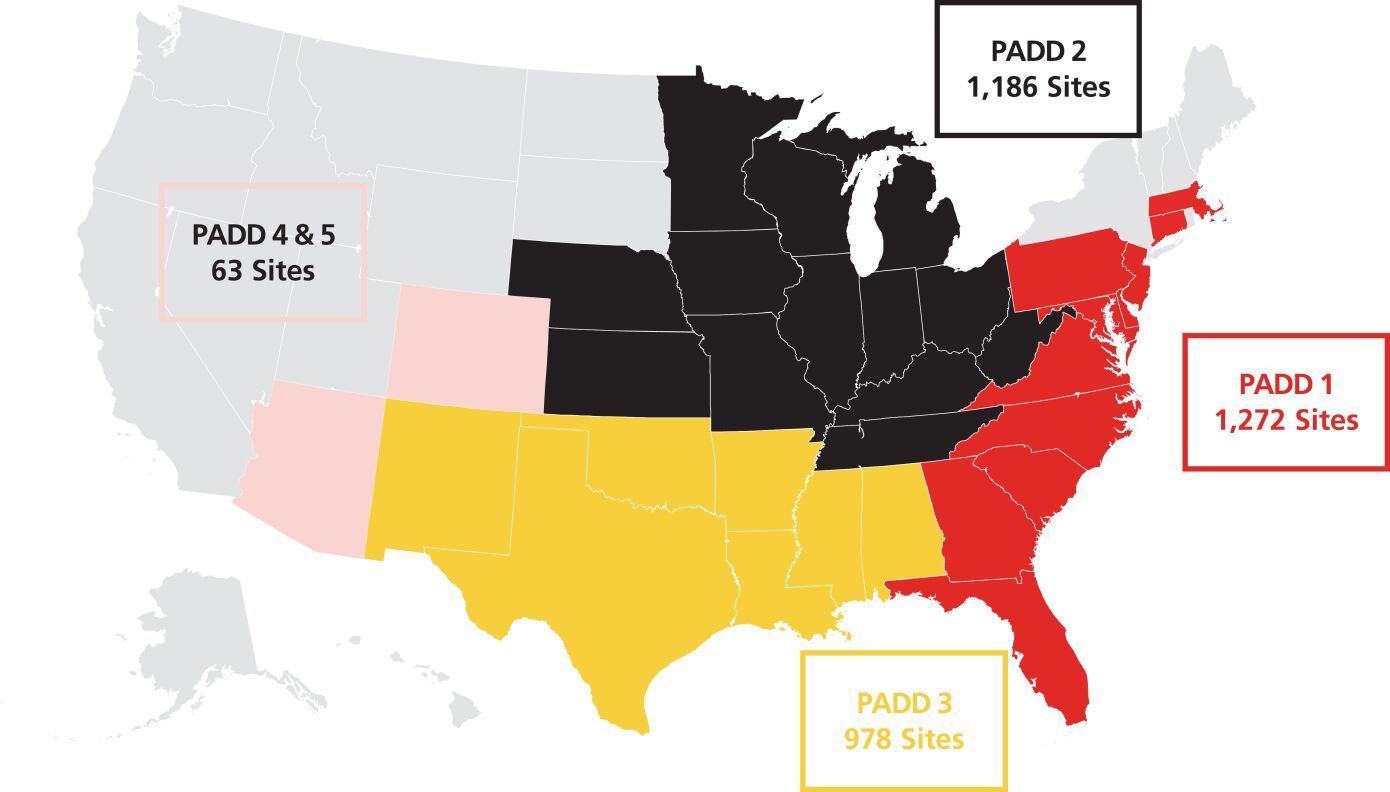

APC Footprint by PADD

Source: Company Data as of 9/30/2025.

Recent Developments

Preliminary Estimated Unaudited Results for the Three Months and Year ended December 31, 2025

We are providing estimates of our preliminary unaudited results for the three months and year ended December 31, 2025. We currently expect that our final results will be consistent with the estimates set forth below, but such estimates are preliminary and our final results could differ from these estimates upon completion of our financial closing procedures due to final adjustments and developments that may arise between now and the time our financial statements for the year ended December 31, 2025 are issued. For example, during the course of the preparation of our financial statements and related notes, additional items that would require adjustments to the preliminary estimated financial information presented below may be identified. These estimates should not be viewed as a substitute for full interim financial statements or full audited financial statements prepared in accordance with GAAP, which will not be filed until after this offering is completed.

Grant Thornton LLP, our independent registered public accounting firm, has not audited, reviewed, compiled or performed any procedures on this preliminary financial information and, accordingly, does not express an opinion or other form of assurance with respect to this preliminary financial information. There can be no assurance that our final results will not differ from this preliminary financial information. Any such changes could be material. Therefore, you should not place undue reliance on these preliminary numbers or assume that they are indicative of what our results for the periods presented will be.

EBITDA and Adjusted EBITDA are non-GAAP financial measures and are not intended to replace financial performance measures determined in accordance with GAAP, such as net income. These non-GAAP measures have limitations as analytical tools and should not be considered in isolation or as a substitute for, or an alternative to, net income or any other financial measure calculated in

21

Table of Contents

Prospectus Summary

accordance with GAAP. For a description of how we define EBITDA and Adjusted EBITDA, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Use of Non-GAAP Measures.”

| For the Three Months Ended December 31, 2025 |

For the Year Ended December 31, 2025 |

|||||||||||||||||||||||

| For the Three Months Ended December 31, 2024 |

Low Estimate |

High Estimate |

For the Year Ended December 31, 2024 |

Low Estimate |

High Estimate |

|||||||||||||||||||

| Actual | Actual | |||||||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| Net income |

$ | 7.5 | $ | 4.1 | $ | 7.4 | $ | 40.2 | $ | 28.8 | $ | 32.1 | ||||||||||||

| Interest and other financing expenses, net |

9.9 | 11.1 | 11.1 | 36.7 | 42.1 | 42.1 | ||||||||||||||||||

| Income tax expense |

2.1 | 1.5 | 3.3 | 15.1 | 10.0 | 11.8 | ||||||||||||||||||

| Depreciation and amortization |

12.6 | 15.2 | 13.2 | 46.1 | 55.8 | 53.8 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

32.1 | 31.9 | 35.0 | 138.1 | 136.7 | 139.8 | ||||||||||||||||||

| Acquisition costs (a) |

— | 0.1 | 0.1 | 0.1 | 0.5 | 0.5 | ||||||||||||||||||

| Initial public offering costs (b) |

— | 0.9 | 0.9 | — | 0.9 | 0.9 | ||||||||||||||||||

| Loss on disposal of assets and impairment charges (c) |

2.1 | 1.9 | 1.9 | 0.8 | 4.6 | 4.6 | ||||||||||||||||||

| Share-based compensation expense (d) |

0.4 | 0.4 | 0.4 | 0.9 | 1.0 | 1.0 | ||||||||||||||||||

| Taxes (received) paid in arrears (e) |

— | 0.1 | 0.1 | (0.6 | ) | 0.2 | 0.2 | |||||||||||||||||

| Adjustment to contingent consideration (f) |

1.0 | (0.4 | ) | (0.4 | ) | — | (2.2 | ) | (2.2 | ) | ||||||||||||||

| Other (g) |

(0.1 | ) | 0.5 | 0.4 | (0.1 | ) | 0.3 | 0.2 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 35.5 | $ | 35.4 | $ | 38.4 | $ | 139.2 | $ | 142.0 | $ | 145.0 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Fuel gallons sold |

524.7 | 489.6 | 489.6 | 2,131.7 | 2,005.8 | 2,005.8 | ||||||||||||||||||

| (a) | Eliminates costs incurred that are directly attributable to business acquisitions and salaries of employees whose primary job function is to execute our acquisition strategy and facilitate integration of acquired operations. |

| (b) | Eliminates costs incurred related to this offering. |

| (c) | Eliminates the non-cash loss from the sale or disposal of property and equipment, the loss recognized upon the sale of related leased assets and impairment charges on property and equipment and right-of-use assets related to closed and non-performing sites. |

| (d) | Eliminates non-cash share-based compensation expense related to ARKO Parent’s equity incentive program in place to incentivize, retain, and motivate our employees. |

| (e) | Eliminates the receipt and payment of historical fuel, franchise and other tax amounts for multiple prior periods. |

| (f) | Eliminates fair value adjustments primarily related to the contingent consideration owed to the seller for the 2020 Empire Acquisition (as defined herein). |

| (g) | Eliminates other unusual or non-recurring items that we do not consider to be meaningful in assessing operating performance. |

22

Table of Contents

Prospectus Summary

Controlled Company Status

For purposes of the Nasdaq rules, we are a “controlled company,” meaning a listed company over which more than 50% of the total voting power is held by an individual, group or another company.

ARKO Parent will hold 94.3% of the total voting power of both classes of our common stock outstanding after this offering (or 93.5% of the total voting power of both classes of our common stock if the underwriters exercise their over-allotment option to purchase additional shares of Class A common stock in full) and will therefore have the ability to determine all matters requiring approval by our stockholders, including the election of our directors, amendment of our governing documents, and approval of certain major corporate transactions (see “Risk Factors—Risks Related to the Transactions and our Governance Relationship with ARKO Parent—ARKO Parent controls our Company and will have the ability to control the direction of our business”). As a result of the voting power held by ARKO Parent, we are eligible for exemptions from certain Nasdaq corporate governance requirements.

Under these rules, a controlled company may elect to be exempt from certain corporate governance requirements. We do not currently expect or intend to avail ourselves of the exemptions available for controlled companies under Nasdaq rules. However, our decision not to rely on the “controlled company” exemptions could change. As a result, you may in the future not have the same protection afforded to stockholders of companies that are subject to all of the Nasdaq corporate governance requirements. See “Management—Controlled Company Exemptions” and “Risk Factors—Risks Related to Ownership of our Class A Common Stock and this Offering—We will be a “controlled company” within the meaning of the rules of Nasdaq and, as a result, will qualify for, and may in the future rely on, exemptions from certain corporate governance requirements. You will not have the same protections afforded to stockholders of companies that are subject to such requirements.”

Summary of Principal Risk Factors

Investing in our Class A common stock involves risks. You should carefully consider the risks described in “Risk Factors” beginning on page 35 before making a decision to invest in our Class A common stock. If any of these risks actually occur, our business, financial condition and results of operations would likely be materially adversely affected. In such case, the trading price of our Class A common stock would likely decline, and you may lose all or part of your investment. Set forth below is a summary of some of the principal risks we face:

| • | The wholesale motor fuel distribution industry and the fleet fueling business are characterized by intense competition and fragmentation, and our failure to effectively compete could adversely affect our business, financial condition and results of operations; |

| • | Our business could be adversely affected by sustained inflationary pressures which may decrease our operating margins and increase working capital investments required to operate our business; |

| • | Significant changes in demand for fuel-based modes of transportation and for trucking services could materially adversely affect our business; |

| • | We depend on several principal suppliers for our fuel purchases and third-party transportation providers for the transportation of most of our motor fuel. A failure by a principal supplier to renew its supply agreement, a disruption in supply, a significant change in supplier relationships or a significant incident related to a supplier could have a material adverse effect on our business and results of operations; |

23

Table of Contents

Prospectus Summary

| • | A significant portion of our revenue is generated under fuel supply agreements with dealers that must be renegotiated or replaced periodically. If we are unable to successfully renegotiate or replace these agreements, then our results of operations and financial condition could be adversely affected; |

| • | If our acquisitions are not on economically acceptable terms, or if our acquisitions do not perform as we expect, our future growth may be negatively impacted; |

| • | The distribution, transportation and storage of motor fuels is subject to environmental protection and operational safety laws and regulations, business interruptions and inherent hazards and risks that may expose us, our customers or suppliers, to significant costs and liabilities, which could have a material adverse effect on our business; |

| • | We are subject to extensive tax liabilities imposed by multiple jurisdictions that potentially have a material adverse effect on our financial condition and results of operations; |

| • | The loss of key senior management personnel or the failure to recruit or retain qualified senior management personnel could materially adversely affect our business; |

| • | Significant disruptions of information technology systems, breaches of data security or other cybersecurity incidents, or compromised data could materially adversely affect our business; |

| • | We will remain a restricted subsidiary and guarantor under the Senior Notes Indenture (as defined herein) upon completion of this offering and will be subject to various covenants under such indenture, which may adversely affect our operations; |

| • | The agreements governing our indebtedness contain various restrictions and financial covenants that may restrict our business and financing activities; |

| • | Our level of indebtedness, together with ARKO Parent’s indebtedness, the terms of our and its borrowings and any future ARKO Parent credit ratings could adversely affect our ability to grow our business, our ability to make cash distributions to our stockholders and our credit ratings and profile; |

| • | Changes in U.S. trade policy, including the imposition of tariffs and the resulting consequences, may have a material adverse impact on our business, operating results and financial condition; |

| • | ARKO Parent controls our Company and will have the ability to control the direction of our business; |

| • | ARKO Parent’s interests may conflict with our interests and the interests of our other stockholders. Conflicts of interest or disputes between ARKO Parent and our Company could be resolved in a manner unfavorable to our Company and our other stockholders; |

| • | The services that ARKO Parent will provide to us following the initial public offering may not be sufficient to meet our needs, which may result in increased costs and otherwise adversely affect our business; |

| • | If ARKO Parent terminates the Management Services Agreement, or defaults in the performance of its obligations under such agreement, we may be unable to contract with a substitute service provider on similar terms, or at all; |

| • | We may have received better terms from unaffiliated third parties than the terms we will receive in our arrangements with ARKO Parent; |

| • | Certain of our related party agreements limit ARKO Parent’s liability and obligations to us; |

| • | ARKO Parent may compete with us; |

24

Table of Contents

Prospectus Summary

| • | We have no operating history as a separate public company, and our historical financial information is not necessarily representative of the results we would have achieved as a separate public company and may not be a reliable indicator of our future results; |